Ponzi Schemes That Duped Millions

Some of the most sophisticated people on earth have handed over their life savings to fraudsters who had nothing more than a good story and a firm handshake. Doctors, lawyers, celebrities, retirees, charities — none of them immune.

The schemes below share a basic blueprint: early investors get paid with money from newer ones, the operator skims off the top, and everyone else loses when the music stops. But the details? The details are wild.

Charles Ponzi: The Man Who Named The Crime

Before Bernie Madoff, before Allen Stanford, there was Charles Ponzi. In 1920, the Italian-born swindler convinced thousands of Boston residents that he could exploit price differences in international postal reply coupons to generate 50% returns in just 45 days.

The arbitrage theory was real. The profits were not. At his peak, Ponzi was pulling in $250,000 a day — the equivalent of millions today. His office on School Street had lines stretching around the block.

People mortgaged their homes. He became a celebrity, profiled in newspapers, invited to dinners. It collapsed within eight months.

When auditors finally examined his books, they found he would have needed 160 million postal coupons to cover his claims. Only about 27,000 existed worldwide. He served prison time, was deported to Italy, and died broke in Brazil in 1949.

The scheme he ran now carries his name permanently.

Bernie Madoff: The Largest In History

Bernie Madoff ran the biggest Ponzi scheme ever uncovered — $65 billion in fabricated account statements, real losses of around $17 billion, and a fraud that ran for at least two decades, possibly longer.

What made Madoff different was the veneer of exclusivity. He didn’t advertise. You had to be referred. His firm produced impossibly steady returns — around 10 to 12% annually, year after year, even during market crashes.

That consistency was the tell. No legitimate investment strategy produces results that smooth. But for investors, the consistency felt like proof of genius rather than proof of fakery.

Madoff’s clients included banks, hedge funds, charities, and prominent families. Elie Wiesel’s foundation lost $15 million. Kevin Bacon and Kyra Sedgwick lost most of their savings.

The victims numbered over 37,000 across 136 countries. He turned himself in to the FBI in December 2008, after his own sons reported him. He died in federal prison in 2021 at age 82.

Allen Stanford: The Cricket Mogul Who Stole $7 Billion

Allen Stanford built an image so elaborate it bordered on performance art. He sponsored cricket tournaments, had himself knighted in Antigua, and lived in lavish style across multiple countries.

His Stanford International Bank, based in the Caribbean, promised CD returns of 10 to 15% when U.S. banks were offering 4%. Investors from the U.S. and Latin America deposited $7 billion.

The money was supposedly invested in a portfolio overseen by a secret team of analysts. There was no secret team. The money funded his lifestyle, his business ventures, and payments to earlier investors.

The SEC had received tips about Stanford as far back as 1997. It took over a decade of inaction before charges were filed in 2009. Stanford was convicted in 2012 and is serving a 110-year sentence.

Tom Petters: The Retail Arbitrage Lie

Tom Petters told investors he was buying electronics — TVs, laptops — at discount and reselling them to big-box retailers like Costco and Sam’s Club. The returns were good.

The receipts looked real. The retailers had never heard of him. Over 13 years, Petters pulled in $3.65 billion.

The purchase orders were forged. The warehouse shipments never happened. His employees created fake documentation on an industrial scale.

The whole operation was sustained by a rotating cast of investors who, by and large, trusted the paperwork more than they investigated the underlying business. When a close associate turned FBI informant in 2008, the operation unraveled fast.

Petters was convicted in 2009 and sentenced to 50 years in prison.

Scott Rothstein: The Lawyer Who Sold Fake Settlements

Scott Rothstein was a well-connected Fort Lauderdale attorney who sold investors a piece of something genuinely appealing: pre-settlement agreements in confidential lawsuits. The victims, he claimed, needed cash upfront and were willing to sell their future payouts at a discount.

Investors would buy a $10 million settlement stake for $6 million and collect when the case resolved. The only problem was that the settlements didn’t exist. Rothstein fabricated court documents.

He forged judicial signatures and created a $1.2 billion fiction that ran from 2005 to 2009. He also had a side operation: bribing law enforcement and cultivating political connections.

When the scheme collapsed, Rothstein fled to Morocco, returned voluntarily, and became a government cooperator. He received a 50-year sentence but has reportedly provided substantial assistance to federal prosecutors.

Reed Slatkin: The Scientology Connection

Reed Slatkin was a co-founder of EarthLink and an ordained Scientology minister. Between 1986 and 2001, he ran a $593 million fraud targeting friends, church members, and wealthy acquaintances.

He claimed to have a proprietary investment strategy with extraordinary returns. In reality, he deposited client money into personal accounts and sent falsified statements.

The fraud stayed hidden partly because Slatkin’s victims trusted him through their shared religious community, and partly because he paid enough early investors to keep word of mouth positive.

When the scheme collapsed in 2001, the Church of Scientology itself was implicated as a beneficiary of Slatkin’s stolen money, though it denied knowledge of the fraud.

Slatkin received a 14-year sentence and cooperated with authorities to recover funds.

Lou Pearlman: The Pop Music Impresario

Lou Pearlman created the Backstreet Boys and *NSYNC, which would be enough of a legacy for most people. But Pearlman was also running a $300 million Ponzi scheme on the side for over two decades.

He sold investments in two companies — FDIC-insured savings accounts and shares in a charter aviation business — neither of which actually existed. He produced fake bank documents, fake FDIC certificates, and fake audits.

Investors included retirees, church congregations, and local businesses in the Orlando area. The scheme began in the 1980s, long before Pearlman was famous.

Fame just gave him more credibility to exploit. He was convicted in 2008, received a 25-year sentence, and died in federal custody in 2016.

Paul Burks And ZeekRewards: Crowdsourcing The Fraud

ZeekRewards was presented as a profit-sharing program tied to an online penny auction site called Zeekler. Participants could earn a daily share of the site’s profits by posting ads and recruiting new members.

It was marketed as a home-based business opportunity. By 2012, ZeekRewards had over a million participants across 200 countries who had collectively poured in nearly $900 million.

The penny auction barely functioned. Most of the “profits” being shared were simply the deposits of incoming participants. The SEC shut it down in August 2012.

It became one of the largest Ponzi scheme cases in U.S. history at the time. Founder Paul Burks paid a $4 million settlement and cooperated with authorities.

Thousands of participants who had recruited friends and family were themselves named as net winners required to return funds.

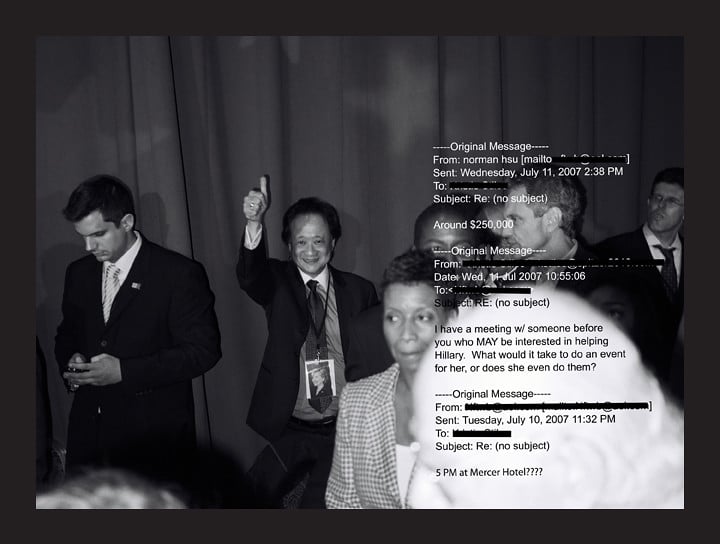

Norman Hsu: Bundler And Fraudster

Norman Hsu was a fashion industry figure who became a prominent Democratic Party fundraiser, bundling donations from others and gaining access to politicians at the highest levels.

He raised millions for Hillary Clinton’s campaigns and was photographed with a roster of public figures. He was also, it turned out, a convicted felon who had skipped bail in California in 1992.

While avoiding that conviction, he ran a $60 million Ponzi scheme, promising investors 40 to 60% returns on investments in a clothing business. After his old California case resurfaced in 2007, Hsu jumped bail again.

He was recaptured on a train in Colorado and eventually received a 24-year federal prison sentence. The political donations raised under his name became deeply embarrassing for the campaigns involved.

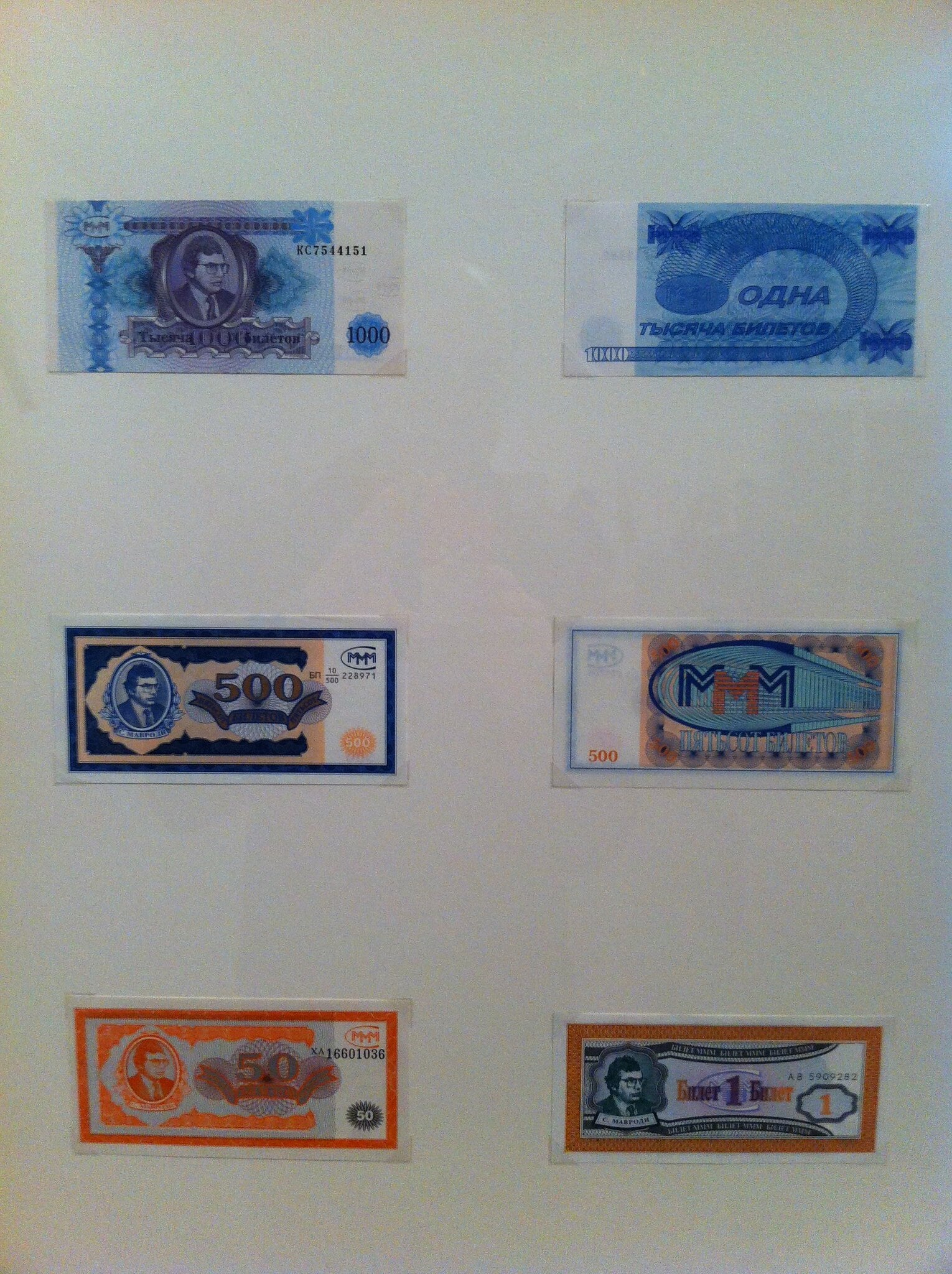

Sergei Mavrodi And MMM: The Soviet Pyramid

Sergei Mavrodi launched MMM in Russia in 1994, and at its height, an estimated 10 to 15 million Russians had invested. The scheme promised returns of 1,000% annually.

No underlying business. No product. Just the promise that your money would grow. MMM became a cultural phenomenon. State television ran ads.

The scheme had its own currency — “Mavrodi Privatization Checks” — and Mavrodi himself was elected to the Russian parliament, which temporarily shielded him from prosecution.

When the scheme collapsed, it wiped out the savings of millions of ordinary Russians still adjusting to life after the Soviet Union. Mavrodi was eventually convicted, served time, and then launched new versions of MMM in multiple countries.

He died in 2018 with no apparent remorse.

Ruja Ignatova And OneCoin: The Crypto Twist

A shiny office space helped sell OneCoin as real digital money. Around the globe, Dr. Ruja Ignatova filled rooms with people eager to listen.

Her presence, bold and magnetic, made headlines wherever she went. Behind the scenes though, no actual blockchain supported the coin. Promises of huge returns lured many into believing they had found gold first.

Those who joined thought they were stepping ahead of another Bitcoin wave. No actual blockchain existed. Running alongside a training program, OneCoin operated like a scoring method.

Inside Ignatova’s network, the tokens meant something — nowhere else did they matter. From 2014 to 2019, people in many nations funneled around $4 billion into the operation.

Flying out of Sofia in 2017, she disappeared mid-route to Athens. Still missing today, her name stays on the FBI’s top-ten fugitive list.

After her exit, control shifted to Konstantin Ignatov — her brother — until arrest brought cooperation. Legal counsel for the operation ended up serving a decade behind bars. As for Ruja, no trace has surfaced since.

Bitconnect Where Hype Masked Risk

Starting in 2016, Bitconnect promised steady profits through a supposed automated trading system built on price swings. Instead of keeping Bitcoin, users gave it to the platform, getting BCC coins back as a substitute.

Those digital tokens climbed in value alongside the main scheme’s claims. For a time, its total value ranked within the highest ten crypto assets worldwide. Tears rolled down faces in ads.

Happiness sparked by sudden profits. Those who pulled in crowds got extra perks from the program. Shutters came down fast after legal warnings arrived from two states that winter.

Almost everything vanished from the token price in a single night. Federal authorities charged founder Satish Kumbhani in 2022 over a scheme involving $2.4 billion.

Since then, he has vanished without a trace.

Joel Steinger And Mutual Benefits Corporation Profiting From Death

A company called Mutual Benefits Corporation dealt in life insurance policies bought cheap from seriously sick people, waiting until those people passed away before collecting. This type of deal actually existed.

But Steinger twisted it into something false. A spokesperson said doctors had signed off on customer plans, claiming each person would live just a short time more.

Yet most reports never came from real evaluations — numbers got made up to pull in funds. When people stayed healthy past their predicted dates, cash ran low fast.

Fresh investments kept arriving, filling gaps left by promises built on false timelines. By 2004, when regulators closed Mutual Benefits, the company had collected well over a billion dollars from nearly thirty thousand people.

Ranking it among the biggest frauds until Madoff surfaced. Twenty years behind bars was the outcome for Steinger.

The People Who Nearly Knew What Was About To Happen

Almost always, a warning came long before things fell apart. Back in 2000, Harry Markopolos sent the SEC a 17-page report saying Madoff’s numbers could not be real — they defied basic math.

Then again, he reached out in 2001, later in 2005, once more in 2007, and yet another time in 2008. Nothing moved at the agency — silence each time.

Funny how some warnings just fade away. Tips about Allen Stanford landed on regulators’ desks back in 1997.

People inside different companies saw odd behavior — yet said nothing, since money kept flowing their way. Reporters poked around once in a while, asking sharp questions that got brushed aside like dust.

Silence held strong for years. Over and over, it happens again. Scammers win by tapping into instincts we all have.

Trusting figures in charge plays a part. So does worrying you’re falling behind. Believing others already checked things? That helps too.

Push those buttons on purpose, attention fades. Even cautious minds slip through the cracks.

Simplicity stands between you and trouble. Not brilliance, not constant worry.

Knowing your investments helps more than cleverness ever could. Question profits that float free of real value beneath them instead.

A slick story? That means dig deeper every time.

More from Go2Tutors!

- The Romanov Crown Jewels and Their Tragic Fate

- 13 Historical Mysteries That Science Still Can’t Solve

- Famous Hoaxes That Fooled the World for Years

- 15 Child Stars with Tragic Adult Lives

- 16 Famous Jewelry Pieces in History

Like Go2Tutors’s content? Follow us on MSN.